The Real Estate (Regulation and Development) Act, 2016 (RERA) was introduced to bring transparency, accountability, and discipline to the real estate sector. While developers, promoters, and allottees are directly impacted, a less-discussed yet critical stakeholder in ensuring RERA compliance is the Chartered Accountant (CA).

From certifying financial statements to ensuring fund utilization from Separate Accounts, CAs are indispensable in making RERA work on the ground.

This blog explores the roles, responsibilities, and statutory requirements placed on Chartered Accountants under the RERA framework.

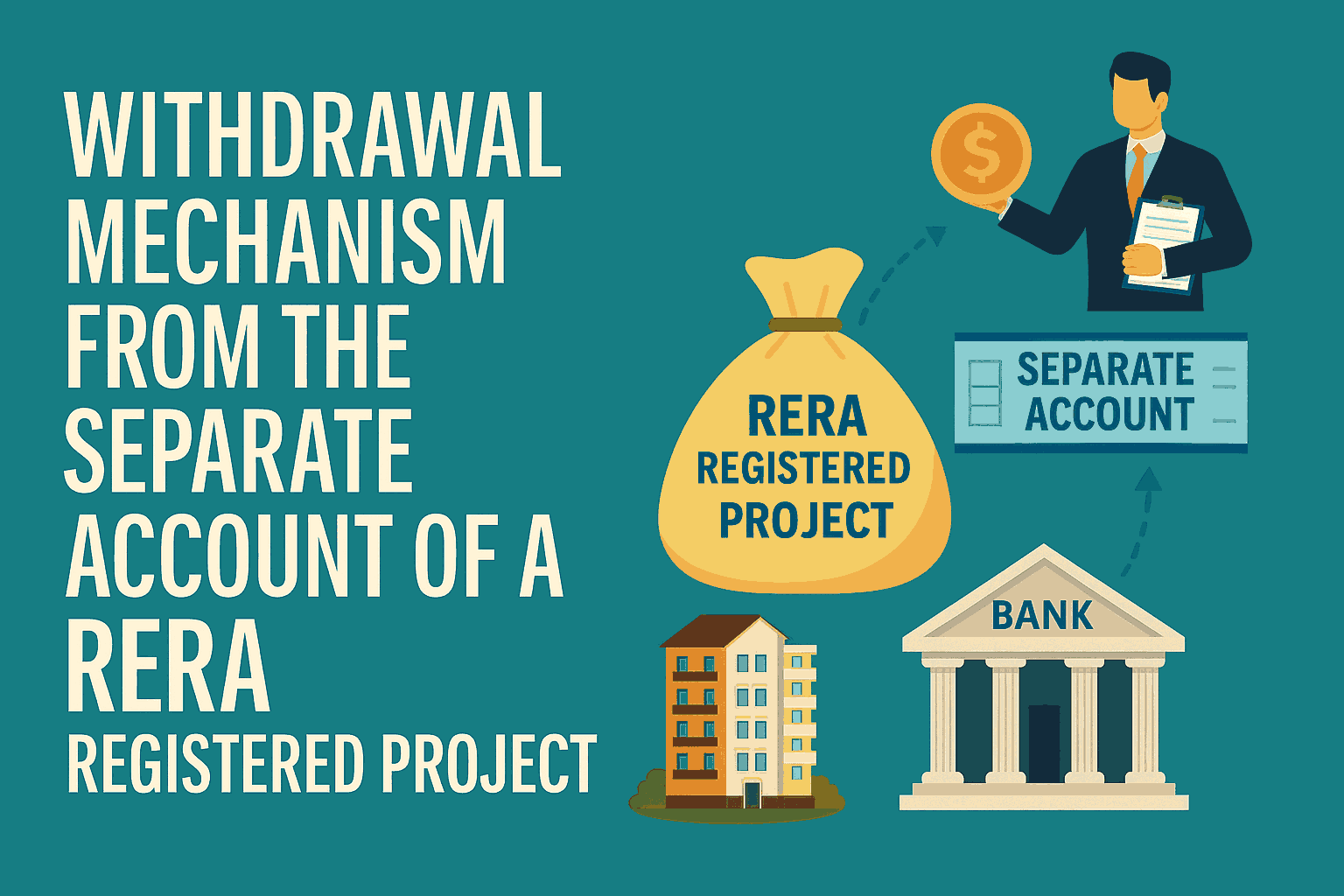

Under RERA, 70% of the amounts realized from allottees must be deposited in a Separate Account. Withdrawals from this account are regulated, and can only be made in proportion to the percentage of project completion.

Role of CA: A Chartered Accountant must certify that the amount being withdrawn is in proportion to the percentage of completion of the project.

Form Used: Form REG-3, Form 3, Form 5, Annexure 3 etc (as prescribed by the respective State RERA).

Purpose: To ensure that funds are not diverted for purposes unrelated to the specific project, thereby protecting homebuyers' interests.

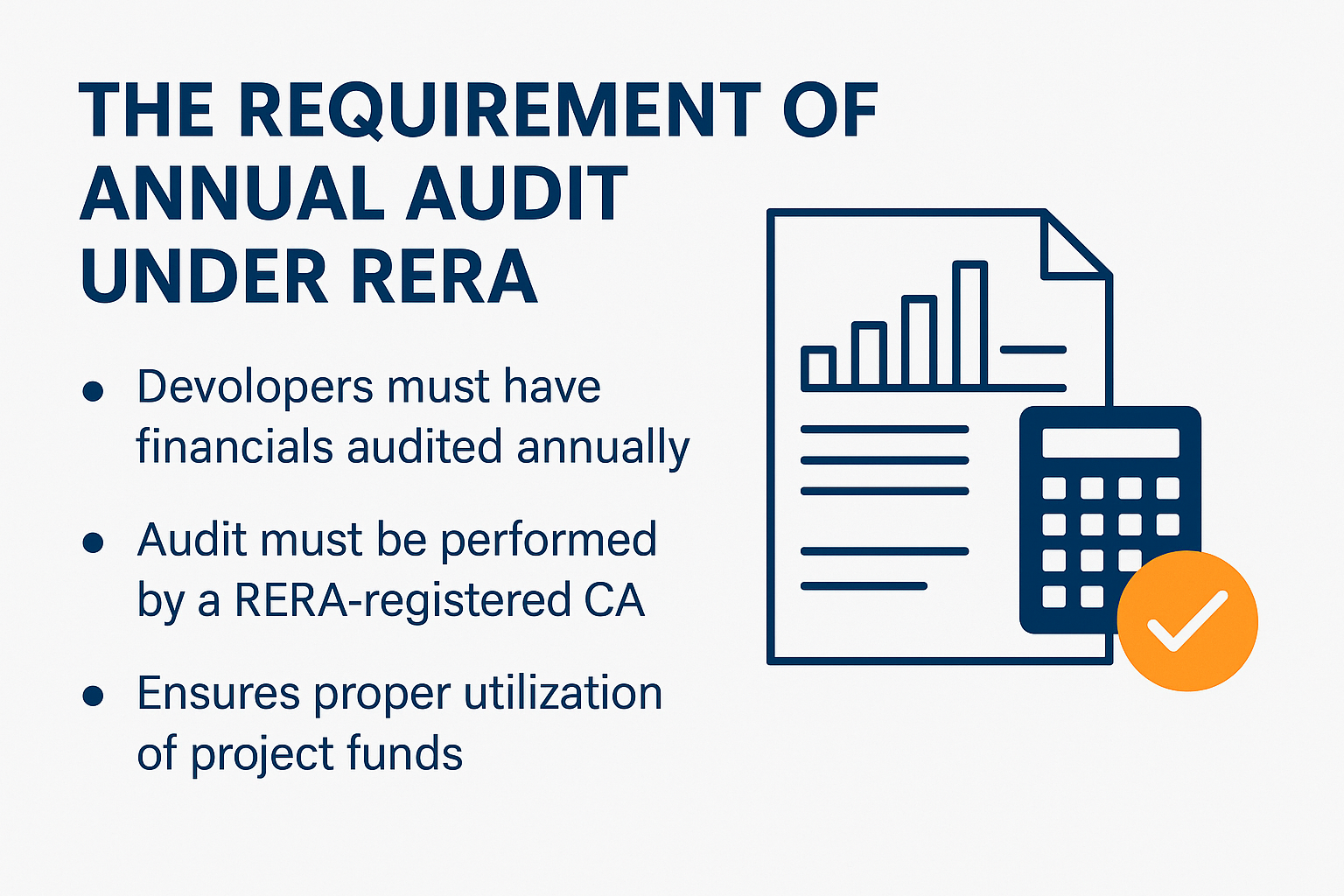

As per Section 4(2)(l)(D) of the Act, every developer must get the project accounts audited within six months after the end of each financial year.

Role of CA: To verify and certify:

That the amounts collected for a particular project have been utilized only for that project.

That withdrawals from the Separate Account are in line with the proportion of completion.

Form Used: Form REG-5, Form 8, Form 5 etc – Audit Report by a Chartered Accountant.

While promoters are responsible for submitting Quarterly Progress Reports, CAs often assist in collating financial information such as:

Funds received during the quarter.

Expenditure incurred.

Balances in Separate Accounts.

Note: Some State RERAs have built-in formats that also seek declaration or data that CAs typically help to compile and verify.

When a developer seeks an extension of registration or proposes modifications in sanctioned plans, they are often required to submit updated project financials, utilization statements, and cash flow forecasts – all of which involve the CA.

If a financial issue or misuse of funds is raised by a homebuyer or authority, Chartered Accountants:

Assist in preparing replies.

Submit certifications or clarifications.

May appear as representatives or advisors alongside legal professionals.

Once a project nears completion, a CA may:

Help promoters in finalizing the handing over of common areas.

Audit the financial records before the Association of Allottees (AOA) takes over.

Ensure no financial irregularities exist in maintenance charges, advances, or other recoveries.

Real estate is governed not only by RERA but also by:

Income Tax provisions,

GST regulations,

State-specific stamp duty and registration laws,

Accounting Standards (especially Ind AS for large companies).

A CA practicing in RERA must understand:

Construction-linked accounting and revenue recognition,

Escrow/Special Account treatment,

Statutory timelines and formats under different State RERAs,

Digital portal-based submissions (especially for UP RERA, MahaRERA, etc.)

As RERA continues to evolve into a more mature regulatory framework like SEBI or IRDAI, the scope of a CA’s involvement will only expand—offering both responsibility and opportunity in equal measure.

CA Akash Jaiswal

Chief Advisor

Apex RERA Professionals

Contact

Apex RERA Professionals is owned by Realtyedge Professionals LLP.